Mythologized both positively and negatively, the American president Trump (henceforth referred to as: stinky weed…) has ensured that he will attract attention all the more intensely the more he shows his buttocks; like a (nuclear-armed) “Bear.” And so something that happened (and continued to evolve) from his election onwards, in early November 2024, passed by if not unnoticed then certainly uncommented upon: the skyrocketing of the dollar exchange rate of bitcoin. Does the presidency of stinky weed have anything to do with so-called “cryptocurrencies”? Why do a large portion of Silicon Valley company owners seem to worship him? What is their relationship with “cryptocurrencies”? Ultimately: is this something that (could) concern ordinary mortals?

Before we give the answer, some basic clarifications are needed. The so-called “cryptocurrencies”, with bitcoin being the most well-known, were never “currencies” or “coins”!!! They were never “money” or “currency/coin”! The images that have staged/portray the supposed monetary “substance” of them are misleading, and moreover… squared. Firstly, because they corrupt the perception of what “money” is. And secondly, because they distort what algorithms are (and how they can be used), reinforcing the metaphysics of the digital “universe”.

According to a typical explanation, “cryptocurrencies are digital assets produced using algorithms.” Such a definition seems vague, since anything “digital” is created through algorithm(s). However, there is a general (social) inability to conceive of a purely “digital asset” unless it takes some recognizable form—of an image, text, a three-dimensional object, etc. We must therefore say that algorithms generate a kind of “numerical/digital entity” which is generally incomprehensible as such unless it assumes some form that allows it to be perceived, more or less illusorily. This is the serious social problem with accepting “artificial intelligence.” There is no actual “intelligence” in algorithmic production; however, insofar as its output takes forms usually regarded as the result of reasoning, the idea arises that the algorithmic system is intelligent-as-such. Empirically, exactly the same illusion arose for those who witnessed the truly impressive automated hydraulic devices of Hero of Alexandria, two centuries BC: they seemed alive, and so something “living” must be moving them…

That, therefore, the result of a specific sequence of algorithmic operations (called blockchain1) was given the “form of currency” (in relevant images: coins) under the name bitcoin, the “currency of bits,” which one might wish to translate as “the production of money through a complex sequence of binary movements of electrons,” we can consider this clever indeed – but a deception. Not because “bitcoin” does not have materiality as one would expect from any form of money (except figurative ones). It does have it and it provides it! But because this particular materiality is indeterminate to the “common user”; and controllable in ways that escape them. As we will see, this indeterminate yet (in unprecedented ways) controllable materiality of so-called “cryptocurrencies” is considered (certainly in the US) the way out of a heavy and structural crisis of capitalist competitiveness. A kind of “escape,” not forward, but upward; toward the stratosphere:

Last Saturday (July 27, 2024), presidential candidate Donald Trump spoke at the BITCOIN 2024 conference in Nashville, Tennessee, explaining his policies on cryptocurrencies and bitcoin that may be implemented as part of a future Trump administration’s policy. Speaking against a backdrop of a banner from Xapo Bank, an institution that aspires to become the global bridge between bitcoin, the US dollar, and stablecoins, Trump’s speech revealed a political vision that would incorporate these three elements in order to “extend the sovereignty of the US dollar throughout the world.”

The discussion about the threatened dollar has been going on for years, with the petrodollar system having ended and various interstate powerful blocs seeking alternative solutions instead of the dollar as a reserve currency. However, Trump – according to his recent speech – seems willing to use bitcoin as a “lifeboat” for the uncontrolled public debt of the USA, and to unleash the expansion of digital dollar stablecoins to which many countries of the global south resort, as the fiscal policies of the covid period continue to decimate the purchasing power of the vast majority of the global population.

Trump promised, among other things, to “create a framework that will allow the safe, responsible expansion of stablecoins… allowing us to extend the sovereignty of the US dollar throughout the world.” He then argued that as a result of the future embrace of his administration with dollar-backed stablecoins, “America will become richer, the world will become better, and there will be billions and billions of people who will be introduced to the crypto economy and will safeguard their savings in bitcoin.” Bitcoin mining was also at the center of his speech, with Trump claiming that “America will become the undisputed global force in bitcoin mining.” This will further solidify something else Trump touched upon, namely that “the US government is among the largest holders of bitcoin”…

This is what Whitney Webb and Mark Goodwin wrote, among others, on July 29, 20242. But old cannabis is considered trash, so his words could be rather indifferent; or he may have completely misunderstood what “cryptocurrencies” are: a 78-year-old could not be considered a “digital native”!!

a brief history of money and blood

Nor could it explain anything! We have to go back 3 years to start understanding how this particular (but not tangible) and controllable digital asset, which can be falsely perceived as “currency” and can make-america-great-again3:

You have most likely heard of the petrodollar. You may not know the details, but you have heard this term in some history lesson. In a very simple way, the word “petrodollar” is an abstract noun that shows the political and military dominance of the US dollar as the only currency in the oil market. By creating it as the exclusive means of transactions, either as dollars or as (American) government bonds, the US could “quantitatively ease” their ever-expanding monetary supply [the constant printing of dollars…] by directly linking it to the perpetual need for an energy commodity such as oil…

What does this historical “direct correlation” of the US dollar with the oil market mean? In the early 1970s, then-US President Nixon was “constantly printing dollars” to finance the increasingly fierce war that his state was waging in Vietnam. However, he had a serious problem. The dollar was “tied” to a fixed exchange rate with gold (35 dollars per ounce of gold) since the end of World War II; and, with this “locked” exchange rate with gold, it had been imposed as an anchor for all the remaining currencies of the planet, the issuing central banks of which did NOT have gold reserves (since they had entrusted them for safekeeping to the USA…). This meant that in order for Nixon to print more and more dollars, he would have to increase the American gold reserves accordingly – something that was impossible.

It thus “freed” the dollar from its parity with gold; however, this would一方面 produce an inflationary currency and另一方面would lose all international confidence in the exchange value of the American currency! This means that no central bank would hold reserves in (large) quantities of dollars.

The solution that was found was “Machiavellian” but consistent with American imperialism. Washington persuaded Saudi Arabia (which was then the largest oil exporter) to price “black gold” exclusively in dollars. The rest of the producers followed suit. What did this mean? Since all countries bought oil, they had to have large reserves of dollars to pay for it! Therefore, the American dollar maintained its international circulation (and “exchange value”) primarily as the global sole measure-of-value of a strategic capitalist commodity, such as oil. This was the petrodollar.

From that moment (1971) onwards, both the US dollar and all other currencies on the planet (which continued to measure their exchange value through their parity with the dollar) were called fiat currencies. Fiat literally means “as they say”: the exchange value of the dollar (and every other currency) is believed to be what-they-tell-us-it-is. It is understood that the detachment of the dollar from its fixed relationship with gold unleashed its free printing, multiplying the “volume” of dollars circulating globally: from 63.6 billion in January 1971, it reached 7.4 trillion by the end of 2007, shortly before the outbreak of the most recent serious financial crisis.

Goodwin continues in the same article:

… American imperialism has changed clothes many times, wearing blue (“democratic”) and red (“conservative”), but always had the same goal: to make more and more money. The activity in the Middle East, starting with the landing of marines in Beirut in 1958, was an initial act that proved to be a guide…. By directly or indirectly occupying the oil-rich states of the region, the US imposed the international use of the dollar in all oil sales and its derivatives. This allowed the federal central bank (FED) to gradually but steadily expand the “monetary supply” of dollars over 50 years, without any apparent loss of demand. Countries that needed oil throughout Eurasia were forced to first buy dollars to pay for the precious fuel to feed their industrial development. By 1990, the “volume” of dollars in global circulation had reached 3 trillion. In the next 30 years, the US extended their control in one way or another to Iraq, Syria, Lebanon, Saudi Arabia, Jordan, and even Afghanistan. By the fall of 2021, this “volume” had reached 20 trillion dollars…

Such a huge volume of petrodollars in circulation (which “fuels” transactions many times larger, since each dollar is used multiple times over as it changes hands) could not remain solely stockpiled in the vaults of the world’s central banks. As early as the ’70s, another use was found: for them to return partially to the US as loans. Indeed, the Fed could issue dollar-denominated government bonds, knowing they would be easily purchased by all countries that had a surplus of dollars, thus securing a steady flow of loans (and lenders) to Washington. But this way, there was a duplication of the “value” of this internationally used currency: it existed simultaneously as “liquidity” (in the US or elsewhere) and as “government bonds.” Meanwhile, the US external debt (the amount it had borrowed from third parties) was skyrocketing: by the early 2025 (before the “woke” government took office), it had reached 30 trillion dollars—a rather terrifying figure, with a continuous upward trend, which could only be considered “sustainable” (meaning it would eventually be repaid) through the ongoing expansion of money printing and recycling of petrodollars. (Already in 2024, the interest payments alone on this debt exceeded 1 trillion…)

Money in the form of currencies-as-we-know-them (and everything that is “built” on these currencies-as-we-know-them: bonds, stocks, financial “derivatives”, etc.) is a contract. The contract implies that currencies-as-we-know-them have a correspondence, a “coverage”, with real values; with material things that are widely accepted as constituting wealth. Gold was such a “thing” for centuries (and remains so…). Oil succeeded it as the real value (of ultimate use) that “covers” the issued dollars, from the 1970s onward.

It’s hard for someone to digest this since usually (paper)money-as-we-know-it is given a metaphysical “value”, without correlation to any real one. However, it is enough for a crisis of trust in this “value” to occur for the collapse of the convention to begin. This can happen to any money-as-we-know-it if it is inflationary; and it has very serious consequences, not abstractly “economic” but (also) social.

This crisis of confidence can happen anywhere. But what if it happens to the American dollar?

The withdrawal of trust; and the god from the machine?

Regarding the international circulation of the U.S. dollar, confidence began to be shaken already from the outbreak of the most recent financial crisis in 2008–2009. It was subsequently the emergence of a serious productive/capitalist competitor, the Chinese state/capital, which literally “rocketed” during the decade following this crisis, accelerating this destabilization. Ultimately, the economic-type war against competitors—in the case of Moscow in 2022 becoming a clear “weaponization” of the institutions that supported the international circulation of the dollar (such as SWIFT), as well as the seizure of Russian assets (including U.S. Treasuries) totaling a not-at-all-negligible amount of 300 billion dollars—dealt the fatal blow: who can sleep peacefully within the dollar-dominated universe when threatened by any adverse awakening of this currency’s “master”?

Or perhaps to create such a “strategically important commodity” from scratch, with just simple, cheap electrons as raw material? And moreover, a “strategically important commodity” whose ownership, whose property rights, would be predominantly American?

bitcoin (‘n’ friends)

Bitcoin first appeared at the end of October 2008 in a text that was electronically distributed on an encrypted list signed by Satoshi Nakamoto, as a proposal for peer-to-peer electronic payments. It wasn’t exactly a “bolt from the blue”: various attempts at something similar had preceded it during the previous decade, mainly among specialists in “digital currency” and digital cryptography. (Specialists who, let’s say here, especially regarding digital cryptography, had direct connections with secret services). In the introductory abstract of the 9-page text, the presenter with the Japanese name wrote:

A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial institution. Digital signatures would offer part of the solution, but the main benefits would be lost if a trusted third party is still required to prevent double-spending. The network [i.e., the one proposed] timestamps transactions by hashing them into an ongoing chain of proof-of-work, forming a record that cannot be altered unless the work of proof-of-work is redone. Such a chain serves not only as proof of the sequence of events witnessed, but also as proof that it came from the largest pool of CPU power. As long as a majority of CPU power is controlled by nodes that are not cooperating to attack the network, they’ll generate the longest chain and outpace attackers. The network itself requires minimal structure. Messages are broadcast on a best-effort basis, and nodes can leave and rejoin the network at will, accepting the longest proof-of-work chain as proof of what happened during their absence.

For those unfamiliar with electronic cryptography and the issues surrounding the transfer of “digital money,” the above would have seemed (and still seems) incomprehensible. From a political perspective, however, the proposal had merit: transferring money (within or outside quotation marks) electronically, without a “third party” intervening to confirm payment. In other words: payments (transfer of money) without traces.

Who did Satoshi Nakamoto have in mind as interested in such a means of bypassing banks (apart, obviously, from the relevant gigs, and those for purely technological reasons)? Nakamoto himself, who introduced himself as a 36-year-old Japanese, remains completely unknown to mysteriously obscure. The New Yorker wrote two years after the proposal for bitcoin, on October 3, 2011, among other things, the following:

Nakamoto… claimed that he had spent more than a year writing the software, partly driven by his anger over the recent economic crisis. He wanted to create a currency that would be immune to unpredictable economic policies as well as the greed of bankers and politicians. Nakamoto’s invention was entirely controlled by software, which would “release” a total of 21 million bitcoins, almost all within the next twenty years…

…Before bitcoin’s debut, there was no coding file with that name. Nakamoto used an email address and a website that were untraceable. In 2009 and 2010, he wrote hundreds of posts in flawless English, and although he called on other programmers to help him improve the code by corresponding with them, he never revealed any personal details. Then, in April 2011, he sent a note to a programmer saying that he had “moved on to other things.” Since then, he has not been heard from again….

However, it turned out that Nakamoto had a political motive… He had introduced Bitcoin just a few months after the collapse of the global banking sector and published a 500-word essay on traditional fiat currencies [note: such as all currencies after the dollar was unpegged from gold in the 1970s]… “The fundamental problem with conventional currency is the trust required for it to function,” he wrote. “The central bank must have the trust of citizens that it will not devalue the currency, but the history of fiat currencies is full of betrayals of this trust. Banks must be trusted custodians of our money and transfer it electronically, but they lend in waves of credit bubbles while holding minimal reserves.”

«Nakamoto» proposed bitcoin in writing on October 31, 2008. The bankruptcy of Lehman Brothers (which is considered the “official” start of the 2008–2009 financial crisis) occurred just a month and a half earlier, on September 15, 2008. If «Nakamoto» is a real person, who, according to his own statement, had been working on the code for at least a year (that is, roughly, from October 2007 onward), and was able to foresee the upcoming financial crisis so early, then a) he is a prophet, and b) he is an expert in economic theory and monetary theory.

It doesn’t seem particularly convincing to us. Various people (related to bitcoin) also seriously doubt whether this is a real person or the pseudonym of some mechanism – they are not entirely wrong.

In the end, “Nakamoto” did not create “currency” as he claimed. He created something else: “digital asset.”

Speaking generally, money (currency) is a measure of exchange value; therefore, it has a direct relationship with the price of any commodity. This is why, throughout history, some “issuing authority” (either the palace or the central bank) had to guarantee the (at least relative) stability of money. When, for example, there were no paper bills (printing technology did not even exist), and money took the form of coins usually minted by the king with his face on one side, these coins had to contain a certain quantity of gold (for higher-value coins), silver (for medium-value coins), or even copper (for low-value coins)—and the presence of this specific quantity of precious metal within the alloy of the coins was guaranteed precisely by their “issuer.” The palace. Obviously, it was (and still is) the population’s trust in this “issuing authority” (that it does not “steal,” that the money is not “counterfeit”) that plays a crucial role in ensuring price stability and, consequently, economic life, both in the daily lives of citizens and among entrepreneurs. If a currency changes its relationship with commodities (what cost 5 “units of money” yesterday now costs 7 or 3, and tomorrow 10 or 1), chaos will ensue. Even worse if such changes are large and sudden.

In its course, bitcoin experienced so many and such fluctuations (in its “exchange rate” with the dollar) that it proved completely unsuitable as a currency! From this perspective, therefore, Nakamoto was not a great expert in monetary theory. Or perhaps he was a good (and above all: imaginative) expert in the therapy that the dollar would need in the intensifying intra-capitalist competition.

But who would care, especially in the early years, about a “payment medium” that would bypass banks and their control? The answer emerged in practice: organized crime. From the moment bitcoin exchanges were created (converting them to dollars and vice versa), it was an excellent way to move large profits of various mafias and transactions between them, far from the indiscreet eyes (or the precise bribery) of the bankers of the first capitalist world.

If the first advantage of bitcoin for its use as “money” was its uncontrollable circulation, the second was that having a final strictly determined number, a limit on its “issuance”, it would never be at risk from the “monetary expansion” which is the usual temptation of central banks – and thus depreciation.

Rushed is the idea for this second advantage. It’s not only the “increase in the quantity of money” that affects its, let’s put it this way, “exchange value.” Given that the political idea behind bitcoin was exclusively the bipolar (marginal) supply / (free) demand, its “exchange value” (or more accurately stated: the exchange rate / measure of this “exchange value” in relation to a fiat currency, let’s say the dollar) could be affected by fluctuations in demand. Or, even, by “hacks” on its network (which has happened…)

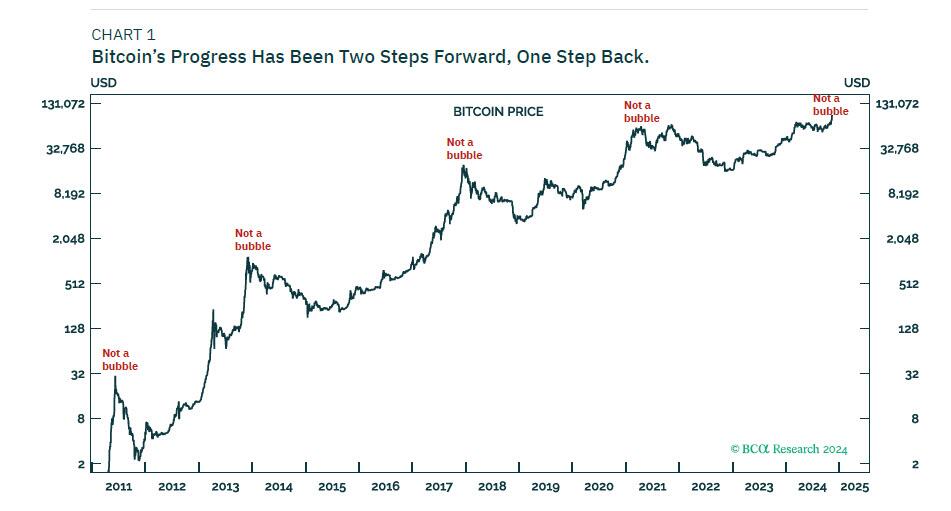

In the long term, and with the right storytelling (hence the artificial increase in demand), bitcoin “rises” as it has been doing so far. The first bitcoin, which was “mined” by the mysterious Nakamoto himself on January 3, 2009, was worth 1 cent, 1/100 of a dollar… On July 20, 2024 (a random date), 1 bitcoin was worth 66,693 dollars. On November 9 (a few days after the American elections and after the victory of the weed candidate was confirmed), 1 bitcoin was worth 76,413 dollars. And on January 19, 2025, 1 bitcoin was worth 105,168 dollars.

But this is the long-term trend. Over shorter time periods, seismic shifts have occurred. For example, in November 2020, $13,000 corresponded to 1 bitcoin. After 4 months, by March 2021, the ratio was $60,000 to 1. Three months later, it had rolled back downward: $33,000 to 1 bitcoin. Dramatic shifts have also occurred within hours. The peak shift occurred on July 19, 2023. At 4:36 AM, the ratio was $301,800 to 1 bitcoin. Ten hours later, at 2:46 PM, it had dropped to $29,807 to 1, less than 10% of the morning’s exchange rate.

Bitcoin may prove unsuitable for everyday transactions. However, having a predetermined electronic limit on its quantity (21 million pieces maximum) it could be excellent as an asset, as a “store of value” – provided there is strong demand for it! If, for example, its dollar “exchange rate” were to rise steadily (and not fall anyway) it could become the asset, the accepted and recognized “financial asset” on which the already (and tomorrow even more) inflated dollar would be anchored.

For bitcoin to become a “significant asset” (instead of “currency”) with an upward “price”, the construction of a permanently strong demand would be needed. For bitcoin to become a “significant asset” reserve upon which the preservation and expansion of the dollar’s planetary hegemony would be based through continuous demand for it, the “significant asset” itself, bitcoin, must have strong demand! That’s how it’s built: to depend on demand!!!

“To increase demand for one thing so that demand for the other will also be maintained or even increased”… What is this called? Squaring the circle with ruler and compass;

If you have printed three trillion dollars that are in circulation (and you want to print more), having a record of its kind that 200,000 dollars or 300,000 dollars or 500,000 dollars correspond to 1 bitcoin makes your dollar look armored – given that bitcoin is amorphous, has no weight or volume, but as a “digital entity” it looks convincing. It inspires trust. It is enough, of course, to possess many, many bitcoins; and to find a way that (forces) others (other states) to seek them while their number is limited.

Is it happening?

stablecoins

This idea, that the dollar will maintain (and even better: extend) its global hegemony as the international measure of exchange value “anchored” not in gold, not in oil or any other strategic (for the 4th industrial revolution) commodity, but in an artificial, digital construct whose main attribute from the perspective of political economy is its strictly limited “volume”, can be considered bold or fetishistic – depending on one’s point of view. It was and remains inadequate, however, for the practical needs of any (geopolitical, economic) hegemon: bitcoin as such, as an “asset”, is not suitable for payments of current transactions, just as square meters of a large real estate property, say of a huge palace, would not do the job either. Above all, though: any advocate of monetary expansion would feel absolutely uncomfortable in the tight suit of the strictly limited “volume” of bitcoins.

So, while the dollar (to be saved) would have to be “anchored” to such a digital entity, something intermediate would also be needed, some kind of “bridge” between the dollar and bitcoins, which on one hand would “resemble” the latter, but on the other hand would have the usage flexibility of the dollar; and, mainly, would follow the increasing “printing” of the latter.

This intermediate something was invented. And it’s called stablecoins!! Stablecoins are also a “digital construct” – but, on the other hand, they have a stable exchange rate with the dollar: 1 to 1!!! By creating a puzzle in the fundamentals of monetary theory, stablecoins have “reserves” of US dollars; which (US dollars) will have bitcoins as their “reserves”! Or they have other stablecoins as their “reserves”! Or they have a digital (algorithmic) mechanism as their “reserves”!… In any case: in contrast to bitcoin, stablecoins DO NOT have a strictly limited “volume” available for any use. Their number can decrease – or increase…

With the greatest naturalness in the world, here is an explanation for stablecoins:

Stablecoins are a category of cryptocurrencies designed to maintain a stable value, in contrast to the high volatility that characterizes other digital currencies, such as Bitcoin. For example, by monitoring the price of bitcoin “live” it is easy to see the intense fluctuations, while stablecoins offer greater predictability.

Stablecoins achieve their stability through various mechanisms. The most common are those backed by reserves in traditional currencies (fiat-backed), such as USD Coin (USDC) and Tether (USDT), which maintain a 1:1 parity with the dollar. Other categories include crypto-backed stablecoins, which are secured by other cryptocurrencies, and algorithmic stablecoins, which use smart contracts to balance supply and demand.

This stability makes them ideal for various applications, such as fast and cheap transactions, protection from inflation, and value storage. However, their operation depends on trust in the inventory management system and the mechanisms that support them, making transparency and compliance with regulations critical.

Someone might wonder: Why all this? Wouldn’t it be simpler and more functional for the American central bank (Fed) to start issuing a digital dollar? Here is the answer/explanation for this fetishism of bitcoin and stablecoins: a) the “digital dollar” would NOT solve the problem of the depreciation of the fiat dollar; and b) the “issuance” of bitcoin and even more so the “issuance” of stablecoins is private!!! The latter, which through their “stability” are offered for transactions, are “issued” by companies; they are, to put it schematically, private money!!!

All supporters of this digital-coins campaign, appearing as saviors of the dollar’s (political / geopolitical / economic) hegemony, are sworn enemies of digital currencies issued by central banks; and fanatical advocates of the idea that this “job” belongs to private enterprises. How do they “sell” this view? With the argument that if “digital money” is issued (and therefore its circulation is controlled) by central banks, then these – that is, the state – will profile citizens through the data of their private transactions; which is, of course, true. They don’t say the rest: that this profiling will be done by companies such as BlackRock, Palantir, Google, X, and the other capitalist mastodons of Silicon Valley!

Here’s how this policy truth is described at the end of 2023 (before crypto appeared on the scene as the dollar-savior) by Peter Howson, a technology researcher and associate professor of international development at the specialized English university of Northumbria, who initially supported cryptocurrencies believing they would help address poverty – until he studied their structure and operation more thoroughly… Through his careful analysis of the process, Howson now considers the “cryptographic economy” overall not just a “bubble” but a mechanism of destruction, capitalism on steroids (“capitalism on steroids”) – a view he presents in his book Let them eat crypto: The blockchain scam that’s ruining the world (Pluto Press, 2023):

The story behind the creation of bitcoin is impressive… Those who created it gathered various technological innovations that had existed for decades. … They are tech enthusiasts and devoted followers of Hayek. They fanatically believe in the views of economist Friedrich Hayek, who supported the idea that any intervention in the functioning of free markets destabilizes what he characterized as “spontaneous order,” a self-regulating system that emerges as a result of individuals’ voluntary actions. They believe that any policy, any government more specifically, must stay away from this beautiful utopia of the free market that will emerge from a system of money creation and circulation that will be cryptographically secure via software.

…The fans of cryptocurrencies promote the idea that digitization and encryption are the formatting of authentic trust – in an era of crisis and lack of trust in existing institutions. They do not care about controlling these institutions. They care about replacing them with codes, the masters of which will naturally be themselves.

…There is something I mention in my book – perhaps not with the gravity it deserved – that is popular among cryptocurrency supporters, and it’s called “the Bitcoin Castle.” The idea is that within the ashes of the impending social collapse, those who early adopted crypto projects will live in bitcoin castles, and the rest will be eternal “no-coiners,” slaves or something similar.

…This culture has a gospel. It is the book by William Rees-Mogg (published 1997) titled The Sovereign Individual: How to Survive and Prosper During the Collapse of the Welfare State. Peter Thiel, one of the promoters of bitcoin [note: member of the “paypal mafia”, now head of the “dirty” Palantir…] wrote the foreword…

When you talk to people who have a direct relationship with the technical aspects of blockchain and cryptocurrencies, software engineers and computer technicians, they are very realistic about the limitations of these technologies. The enthusiasts are (or pretend to be) those who intend to use them to enhance their powers.

… The supporters of these processes use misleading language. They use terms like “decentralization” or “distributed networks” to create the impression of complex actions that ensure the reliability of the technology. In reality, the exact opposite is true. Even more power is concentrated in the hands of people we have no reason to trust. They say other things too. “Don’t be against innovation”! “Don’t stop us from making the world better and fairer through computer code”! But these are smoke screens

Philosopher’s stone

The technofetishism behind these stories doesn’t just whisper. It screams! However, it is called upon to “solve” a real problem. From the article by Webb and Goodwin that we mentioned earlier:

In order for a new Trump administration to successfully meet the demands of Congress’s budget, while at the same time servicing the $35 trillion debt we already owe, the Treasury Department must find a willing buyer for this newly issued debt. Over the past 18 months, a new high-level buyer of this debt has emerged from the cryptocurrency industry: stablecoin issuers. Stablecoin issuers such as Tether or Circle have purchased over $150 billion of U.S. debt—in the form of Treasury securities— in order to “back” their token issuance with a dollar-denominated asset. To put the impressive volume of U.S. public debt these relatively new and relatively small companies have absorbed so far into perspective, China and Japan, historically the largest creditors of the U.S., hold approximately just below and just above $1 trillion, respectively, of the same Treasury bonds. Despite having existed as a company for only about a decade, and despite its market capitalization barely surpassing $10 billion in 2020, Tether has reached the point where it alone holds over 10% of the Treasury bonds held by any major nation or creditor of the U.S.

The use of stablecoin to mitigate the problem of US debt has been circulating as an idea among Republicans for quite some time. Despite his “never again” stance against Trump, former House Speaker Paul Ryan expressed exactly this sentiment in a recent article in the Wall Street Journal titled “Cryptocurrencies Will Prevent a US Debt Crisis.” Ryan claims that “dollar-backed stablecoins offer demand for US public debt” and therefore “a way to keep up with China.” He speculated that “the crisis [of debt] is likely to begin with a failed public auction,” which in turn would lead to “a painful surgical intervention in the budget.” The former House Speaker predicted that “the dollar will suffer a major confidence shock” and as a result asks: “What can be done?” His immediate answer is to “start taking stablecoins seriously.” Dollar-backed stablecoins come as “a significant net buyer of US public debt,” he notes, with stablecoin issuers now being the 18th largest holder of American debt. Ryan continues by saying that “if dollar stablecoin issuers were a country,” this state “would rank just below the top ten US creditor nations,” still lower than Hong Kong but higher than Saudi Arabia, the former US partner in the petrodollar system.

As this industry is set to expand and deregulate under the future Trump presidency, stablecoins—including PayPal’s relatively new stablecoin, PYUSD—could become “one of the largest buyers of U.S. government debt” and, primarily, a “reliable source of new demand” for public bonds. Paul Ryan notes the often-discussed trend of de-dollarization that is exerting pressure on the timeline for expanding this industry, stating that “if other countries manage to strengthen their currencies’ influence while abandoning U.S. public debt, the U.S. will need to find new ways to make the dollar more attractive,” suggesting “dollar-backed stablecoins” as “an answer.”

The techno-fetishism that howls is one side. The financial despair in Washington is the other. The new government of the bankrupt weed is searching, half-blindly and half-by-groping, for the exits of a forward escape: they urgently need assets to support the seriously threatened exchange value of the dollar! Greenland’s minerals? The Panama Canal? Ukraine’s rare earths? Anything!

Within this “anything” cryptocurrencies appear as a magical solution – and the tech billionaires of the once mighty Silicon Valley have aligned themselves behind the digital currency trend because they have much at stake. However, how likely is it that this trick will succeed?

We won’t make a prediction… However, we will recall a heavy shadow that falls upon the combination of technofetishism and insatiable thirst for wealth: it’s called the philosopher’s stone!

It was about a “magical” chemical substance they were seeking (or trying to create) for many centuries, which would basically turn common metals (such as lead, mercury, or tin) into gold; but it would also be the elixir of life and ensure immortality…. The most famous seekers of the “philosopher’s stone” were called alchemists (from the Arabic word al-kimiya), that is, in today’s terminology, chemists. Over time, many were simply frauds; others, however (from Paracelsus to Isaac Newton…), were serious. In the search for this magical substance that was never found, other useful techniques were discovered, such as distillation.

However, the “ideal” behind this pursuit was much more familiar to today’s conditions: the universal control over nature and life as such. The alchemists didn’t make it, but there are however worthy modern continuators of the effort, under different names – since “technology has advanced.”

The search for the salvation of dollar hegemony within bytes and hardcore complex algorithms (: “encryption”) is a contemporary variation of the “philosopher’s stone”…

An elixir-of-life, some kind of immortality for the American empire is up for grabs…

Ziggy Stardust

- More about blockchain in cyborg 14 Blockchain: the protocol of the gods and cyborg 15 Blockchain: towards a legislative technology. ↩︎

- Bitcoin Magazine, Trump Embraces the “Bitcoin-Dollar” Stablecoins to Entrench US Financial Hegemony. H Webb is a journalist. Goodwin is former editorial director of Bitcoin Magazine, and author of the book The Bitcoin-Dollar: An Economic Monomyth. The article is accessible at https://bitcoinmagazine.com/politics/trump-embraces-the-bitcoin-dollar-stablecoins-to-entrench-us-financial-hegemony ↩︎

- Bitcoin Magazine 29 September 2021, Mark Goodwin The Birth of The Bitcoin-Dollar. Available at https://bitcoinmagazine.com/culture/the-birth-of-the-bitcoin-dollar ↩︎